For a long time, investors mostly treated Coke and Pepsi the same way. Defensive consumer names. Predictable cash flow. Stocks people bought when they wanted stability and forgot about when the market turned aggressive again.

That stopped working quite so neatly over the past year.

The conversation around PEP vs KO has shifted away from branding and into something far less visible. Margins. Promotions. Input costs. Pricing tolerance. The numbers inside the earnings reports suddenly matter more than whichever celebrity showed up in the latest commercial campaign.

The old Coca-Cola vs Pepsi market share debate still comes up, especially internationally, where distribution scale remains a real weapon. But after the latest quarter, traders spent less time talking about shelf space and more time looking at who is protecting profitability without damaging demand too badly.

Coca-Cola is making the cleaner case

Coca-Cola’s first-quarter report did not contain much drama. Markets usually like that.

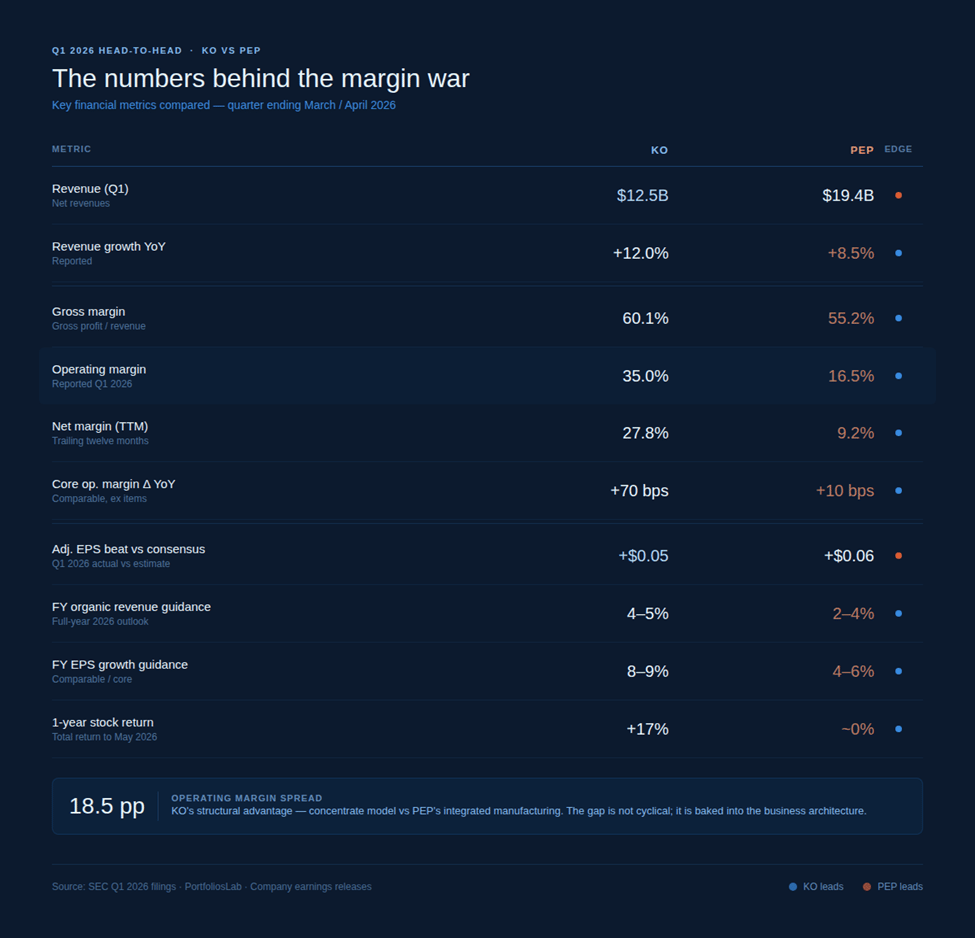

Revenue rose 12% to $12.5 billion. Organic revenue increased 10%. Comparable operating margin moved up to 34.5% from 33.8% a year earlier.

The broader beverage industry competition backdrop helps explain why the market reacted well. Based on trailing comparative data from PortfoliosLab, Coca-Cola entered May with gross margin sitting near 60%. PepsiCo remained closer to 55%.

That gap is structural as much as cyclical.

Coca-Cola simply carries less operational weight. The company depends heavily on concentrated and franchised bottling relationships. PepsiCo has a far messier machine underneath the hood because snacks, transportation, packaging, retail exposure, and manufacturing all move together.

The current KO vs PEP setup reflects that difference pretty clearly.

PepsiCo spent much more time talking about affordability over the last year. Coca-Cola mostly stayed out of that conversation and stuck with higher pricing instead, even as grocery shopping started feeling more calculated for a lot of consumers across North America.

There are signs that the approach is holding up. Coca-Cola Zero Sugar volume rose 13% during the quarter, and the brand still seems to be selling well without needing the kind of discounting other packaged products have started relying on.

Not everything inside the report looked perfect. Tea and coffee input costs remained a problem, according to management commentary. Still, the company raised its comparable EPS growth outlook for 2026 to 8%–9%, which probably mattered more to investors than the commodity discussion itself.

That partly explains the widening Pepsi vs Coca-Cola stock gap over the last year. KO increasingly trades like a steady quality name at a time when investors still do not fully trust the broader consumer backdrop.

PepsiCo Is playing a different game

PepsiCo’s quarter felt more uneven.

The company still beat earnings expectations. Revenue rose 8.5% year over year to about $19.4 billion. But unlike Coca-Cola, the important part of the story was not margin expansion. It was volume stabilization after several rough quarters.

PepsiCo Foods North America reported 2% volume growth in Q1. Management also said the business added around 300 million incremental consumption occasions versus the same period a year ago.

Inside today’s soft drink market competition environment, that matters.

PepsiCo appears more willing to protect demand, even if margins stay under pressure for longer. Coca-Cola, by comparison, still looks more focused on defending profitability first and letting volume follow afterward.

The margin difference between the two companies remains large. PepsiCo reported an operating margin of 16.5% during the quarter, although underlying core operating margin growth stayed relatively modest after adjustments.

That is where the broader Coke vs Pepsi pricing strategy divide becomes easier to see in practice rather than theory.

PepsiCo operates in categories where consumers react quickly to price changes. Snacks especially became more sensitive once food inflation stayed elevated for multiple years. Coca-Cola has a simpler structure and slightly more flexibility to hold pricing without leaning as aggressively on promotions.

The contrast is showing up across wider beverage pricing strategies as well. One company is trying to preserve margin consistency. The other is trying to rebuild volume momentum without losing too much pricing power in the process.

What traders are actually watching

The latest PEP/KO comparison no longer looks like a standard staples trade.

Right now, Coca-Cola looks like the cleaner story for investors. Margins are stronger, guidance has been more stable, and there are simply fewer moving parts to worry about. PepsiCo still has upside if consumer spending in North America starts improving again later in 2026.

That difference has shown up pretty clearly in the stock performance. KO has pulled ahead of PEP over the last year, and the conversation around beverage names now feels less about raw sales growth and more about who is actually running the business better quarter to quarter.

Investors are still keeping a close eye on PepsiCo’s beverage division in North America, especially after the company pushed further into energy drinks and healthier product categories. PepsiCo’s own Q1 materials also acknowledged that stronger second-half demand remains important to the recovery picture.

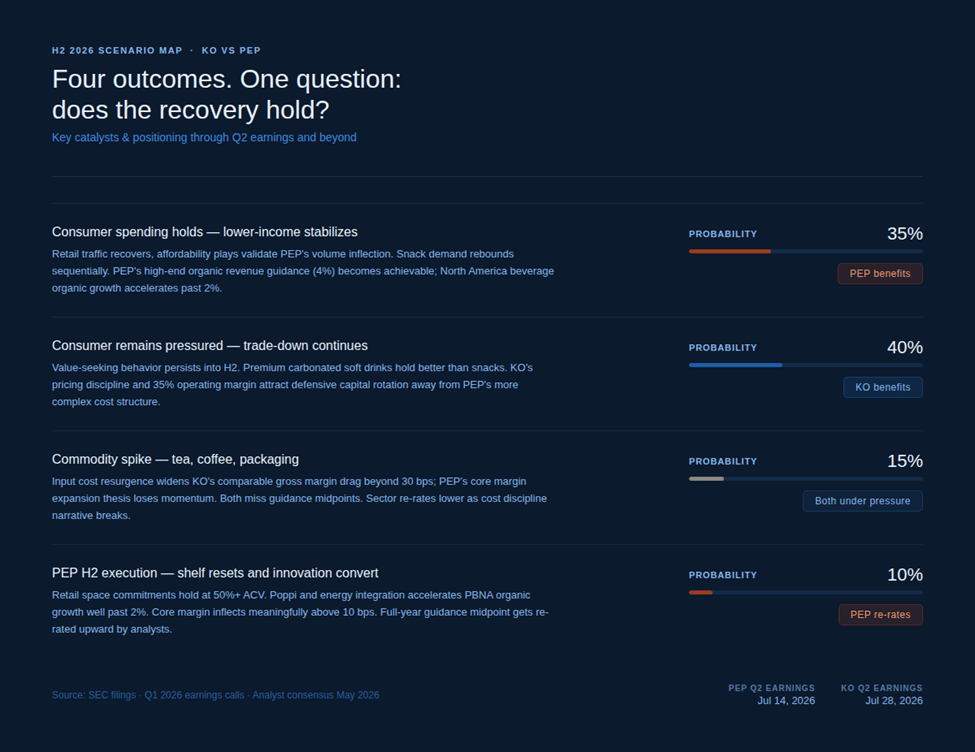

For traders running a Versus Trade PEP KO, the next real test probably arrives with Q2 earnings and updated summer spending data. If lower-income consumers keep pulling back, Coca-Cola may continue attracting defensive positioning. If retail traffic improves, the current trade Pepsi vs Coca-Cola setup could start tilting back toward PepsiCo.

From a broader Pepsi vs Coke financial performance perspective, the market still appears more comfortable rewarding consistency than waiting for a recovery story to fully play out. Whether PepsiCo can rebuild margins without losing the volume improvement it regained this quarter will probably decide how the second half of 2026 trades.