Zee Entertainment Ltd’s ₹2,237 crore preferential share warrant issuance—increasing the Chandra family’s stake from 3.99% to 18.39%—raises fundamental concerns about a company prioritizing control over transformation.

This decision comes as Zee occupies an uncomfortable middle ground between streaming and traditional broadcasting, with mixed financial signals.

Read this | Gaurav Banerjee sets audacious goals to rebuild Sony after failed ZEE merger

Despite improved FY25 results—Ebitda margins rose 390 basis points (bps) to 14.4%—the picture remains concerning: advertising revenues are falling, and ZEE5 continues to lose nearly ₹550 crore in a market where scale determines survival.

FY25 expense management was clearly disciplined: content costs declined 10.4%, employee expenses fell 9.0% year-on-year (YoY), and other costs dropped 16.0%.

But these improvements cannot mask the 11% YoY drop in ad revenues, with domestic advertising plunging 27% in Q4FY25 to ₹779 crore. Management acknowledged in its post-results call that the market remains under pressure—suggesting efficiency gains, not market expansion, are driving the recovery.

In short, Zee’s operational progress reflects defensive cost control rather than growth-oriented reinvention.

Meanwhile, India’s entertainment sector is undergoing rapid transformation. Global streamers are pouring billions into original content, advanced algorithms, and seamless user experiences. Traditional broadcasters, meanwhile, are steadily losing audiences to digital platforms.

Retreat from originals and scale

In streaming, original content is both product and competitive edge – the engine of differentiation and loyalty. Netflix, Disney+, and Amazon Prime Video invest billions annually in exclusive programming that differentiates their offerings and builds loyal audiences.

Larger platforms enjoy three reinforcing advantages:

- Economies of scale: They spread high production costs across vast subscriber bases.

- Data network effects: Larger audiences generate richer behavioural data, powering superior recommendation engines.

- Content bargaining power: Their scale helps secure top-tier content and talent on favourable terms.

ZEE5 lacks that scale. Its relatively smaller user base constrains both its data ecosystem and content budget, making it harder to compete in either user engagement or programming.

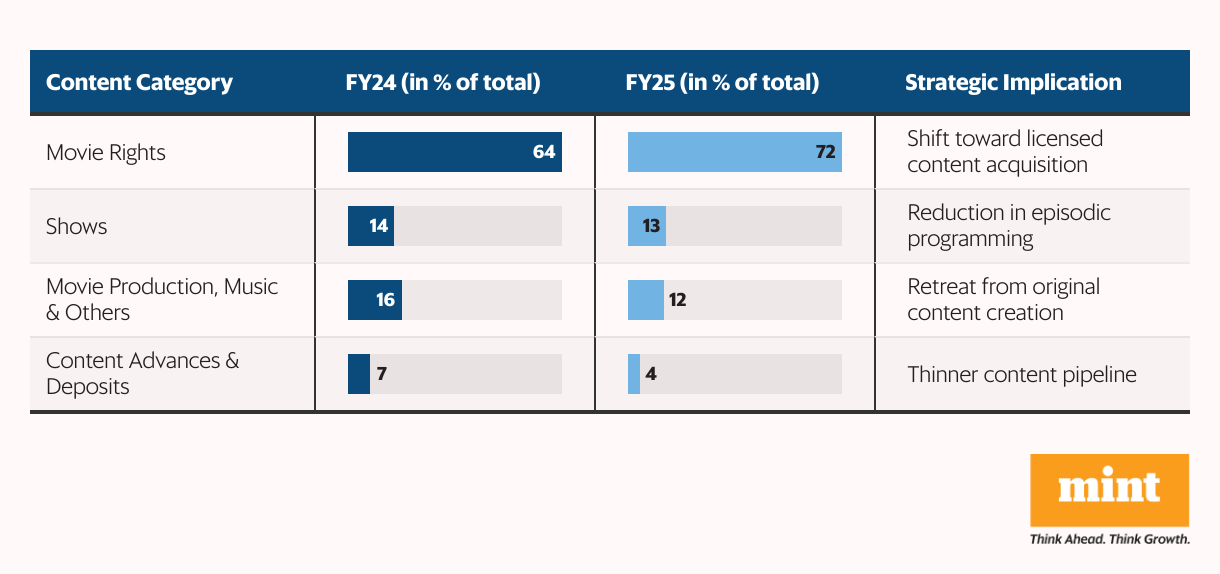

In the past year, Zee’s inventory allocation has shifted sharply — revealing a defensive content strategy with serious long-term implications:

Short-term focus: Licensed content requires less upfront investment and aligns with cost-cutting.

- Weaker differentiation: It lacks the brand identity or stickiness of originals.

- Lower long-term value: Originals build IP that compounds over years; licensed content does not.

- Admitted scale disadvantage: The shift implies Zee knows it cannot match the content investment of global rivals.

- The result: immediate savings, but less content that defines platform identity and audience stickiness.

Read this | Will ZEE5’s new slate of content, regional push, and micro-drama help it win the OTT war?

Zee is retreating to safer territory, prioritizing immediate savings over building the distinctive content needed for long-term relevance in streaming wars.

“New monetisation engines”—or tactical retreat?

Zee appears to have accepted that direct competition in premium streaming is no longer viable.

Chief executive Punit Goenka is now focusing on what he calls “new monetization engines”—FAST (Free Ad-Supported Television) channels, syndication, UGC partnerships, and retail-led advertising models. Zee is also re-entering the free-to-air television segment it previously exited.

This marks a significant retreat. Zee is pivoting to lower-margin models. The move back into free-to-air, once deemed obsolete by Zee itself, signals a scramble for survival over long-term positioning.

Zee’s “Bullet” micro-drama format typifies this tactical repositioning: bite-sized content designed for mobile users with short attention spans. These narratives are cheaper to produce and ad-heavy—but they’re short-lived and face stiff competition from social platforms with better tech and bigger reach.

Unlike premium originals that build IP and long-term subscribers, micro-content struggles to create lasting engagement or durable value.

Strategic crossroads

This situation demands decisive strategic choices. Yet the warrant issuance raises questions about whether Zee is truly exploring alternatives that benefit all stakeholders.

At least three options stand out:

- Digital partnerships: Tie up with global tech players entering Indian streaming, bringing both capital and scale.

- Vertical specialization: Focus on niches where Zee has a brand edge—accepting a narrower but defensible position.

- Strategic consolidation: Consider merger or acquisition paths with larger firms seeking local content assets.

Zee has assets that could power any of these: a vast content library, strong production infrastructure, and broad audience relationships. Tech partnerships could have unlocked funding for new IP and wider distribution. Niche production alliances could have given it brand depth. Geographic expansion might have unlocked new monetisation layers.

Instead, Zee is doubling down on internal control.

Capital allocation reveals priorities

A company’s capital allocation choices often reveal its true strategic focus beyond public statements. With Zee’s shares trading at under 1.2x book value—down from 2.6x in FY23—a share buyback would have signalled management’s belief in long-term value.

The ₹2,400 crore in cash and equivalents at the end of FY25 could easily have supported that. A repurchase would have boosted earnings per share, returned value to all shareholders, and possibly lifted market confidence.

The preference for warrants that significantly increase family ownership suggests governance control takes priority over shareholder returns while making incremental investments across various business segments.

This approach risks leaving Zee undersized in highly competitive markets. It’s consistent with defensive positioning rather than growth optimization, despite management maintaining an ambitious Ebotda margin target for FY26.

Read this | Zee and Sony split up. Now, streaming studios are sulking

Some analysts have upgraded their view on Zee based on improvement in operating performance and projected earnings recovery—the share was up 10.5% on 23 June from its previous close, and over 34% from 8 May when FY25 results were announced. But the fundamental strategic question remains: How can it create sustainable value in a sector increasingly dominated by global platforms with superior scale?

Meaningful transformation would require substantial content investment, strategic partnerships providing scale advantages, or technological innovation enhancing user experiences. Initiatives like “Bullet” represent creative adaptation but fall short of the structural changes needed to reposition the company for long-term growth.

Analysts forecast ad revenue will rise on FY25’s low base, which they project will drive expansion in Ebitda margin over the next two years given the cost reset. However, this improvement relies more on operational efficiency than market expansion or strategic reinvention.

For more such analysis, read Profit Pulse.

The decision to issue dilutive warrants rather than pursue shareholder-aligned capital strategies suggests a company focused more on control than transformative growth, even as it achieves notable operational improvements through cost management.

By operating between heavyweight streamers and niche players, Zee risks becoming neither. Without radical reinvention or clear specialization, it may find itself trapped in a slow-moving squeeze—less a content creator than a distributor, more a legacy operator than a future leader.

About the author: Dev Chandrasekhar advises corporations and think-tanks on big picture narratives relating to strategy, governance, markets, and policy.

Disclaimer: The author does not own any shares or derivatives, if any, of the shares of Zee Entertainment Enterprises Ltd and is not associated in any pecuniary or advisory capacity with Zee, its owners, its employees, or its competitors. The article is a forward-looking interpretation of publicly available information on strategy and governance; it does not offer any investment advice related to any company. Any factual error, if pointed at, shall be corrected. No liability accepted.