Coca-Cola (KO) posted its Q2 2025 results with a headline EPS beat, but the quality of that beat warrants a closer look. Below is a breakdown of the key financial metrics and what truly drove the performance, followed by an analysis of the current technical setup in KO’s stock price.

Headline numbers (Non-GAAP Focus)

| Metric | Actual (Q2 2025) | Consensus | Y/Y Growth |

| EPS (Non-GAAP) | $0.87 | $0.83 | +4% |

| Revenue | $12.5B | $12.5B | +1% |

| Organic Revenue | +5% | — | +5% |

| Operating Margin (Adj) | 34.7% | 32.8% | +190 bps |

What drove the beat?

1. Margins, Not Revenue, Powered the EPS Beat

Coca-Cola matched revenue expectations but surpassed EPS estimates by 4 cents. The driver? Margin expansion.

-

Adjusted operating margin jumped 190 basis points to 34.7%.

-

On a currency-neutral basis, margins were even stronger at 36.0%.

This was primarily due to:

-

Tight control over SG&A expenses

-

Deferred marketing investments

-

Eased input cost pressures

-

Effective pricing strategies

Conclusion:The beat was operational, not volume-based. EPS strength came from internal efficiency, not external growth.

2. Weak Volume Points to Soft Demand

The underlying demand picture wasn’t encouraging:

-

Global Unit Case Volume:–1%.

-

Coca-Cola Trademark:–1%.

-

Juice/Dairy/Plant-Based:–4%.

-

Asia-Pacific:–3%.

-

Latin America:–2%.

This suggests Coca-Cola’s growth was driven byprice/mixrather than more product being sold.

Conclusion:There’s a vulnerability here. If inflation continues cooling or if promotional spend increases, price/mix benefits may erode quickly.

3. FX Was a Drag, but Margins Held Firm

While currency effects shaved 5% off EPS, Coca-Cola still delivered+9% EPS growthon a currency-neutral basis. That reinforces the company’s strong operational execution.

4. Negative Free Cash Flow — But Explained

Free cash flow was–$2.1B, but this included a$6.1B payment for fairlife. Excluding that, adjusted FCF was a healthy+$3.9B.

This isn’t a red flag unless negative cash flow persists into future quarters.

5. Slightly Upbeat Outlook

Coca-Cola guided full-year comparable EPS growth to+3%, reaffirming 5–6% organic revenue growth. The modest upgrade reflects confidence in margin control, though not necessarily volume growth.

Second-order view: How strong was the beat, really?

-

Quality of Earnings Beat:High. It wasn’t propped up by lower taxes or buybacks—this was real operational discipline.

-

Risks:Negative global volume is a red flag. If price/mix stops working, growth could flatline.

-

Investor Perception:Depends on positioning. Those expecting a demand rebound may be disappointed. However, those valuing margin control and cost discipline may stay bullish.

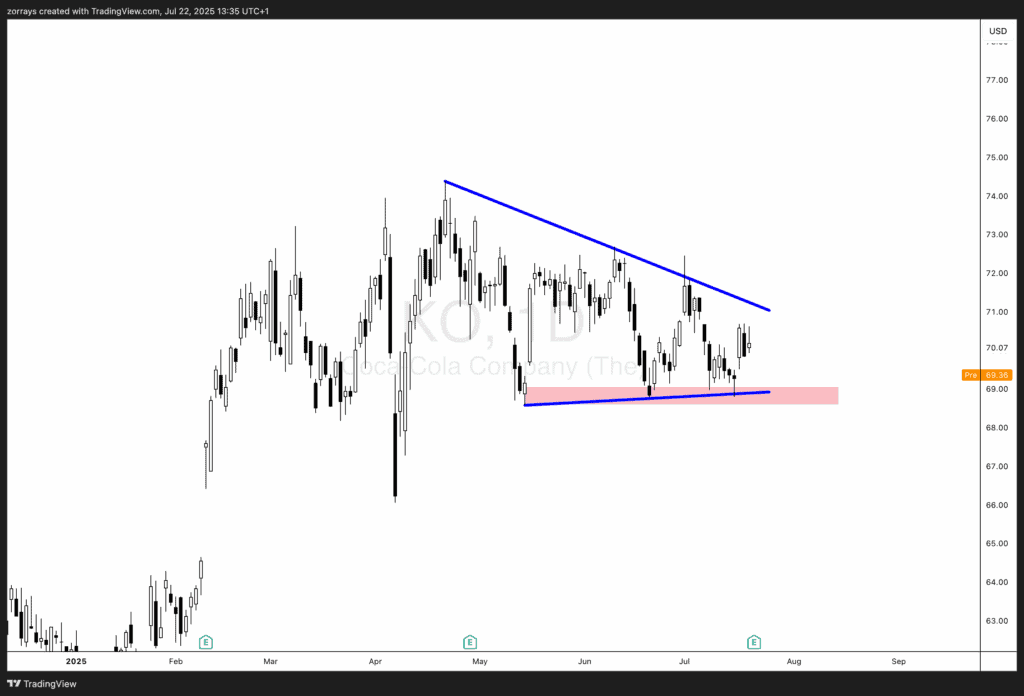

Technical analysis: Compression near a critical level

Coca-Cola’s stock is currently consolidating inside asymmetrical triangle, withdescending highs and a flat support zone around $69, highlighted in red.

What to Watch Technically:

-

The$69 levelhas held multiple times, acting as a firm support.

-

This zone aligns with previous demand accumulation and could represent buyer interest.

-

However, the stock is nearing theapex of the triangle, and compression usually precedes a breakout or breakdown.

Scenarios Ahead:

-

Bullish Case:If KO continues to respect $69 and breaks above the descending trendline (~$71), it could trigger a move toward$73–$75, driven by renewed optimism in margin control and potential Q3 marketing reinvestment.

-

Bearish Case:A confirmed breakdown below $69 opens the door to a drop toward$66, a prior area of consolidation from early 2025.

Catalyst Needed?

Fundamentally, Coca-Cola will need either:

-

A turnaround inunit volume growth.

-

Clearmarketing spend deployment plansto drive future demand.

-

A shift in sentiment where investors rewardmargin protectionover volume growth.

Until then, $69 remains amake-or-breaklevel. A close below that support—especially on volume—would raise caution.

Final thoughts

Coca-Cola’s Q2 2025 performance was a masterclass in cost and margin management, but it did little to ease concerns about consumer demand. The market’s response may hinge on how much slack investors are willing to cut a high-margin, slow-growth business in a soft macro environment. Meanwhile, from a technical standpoint, all eyes should remain on the $69 level—if that breaks, KO may have further downside to explore.