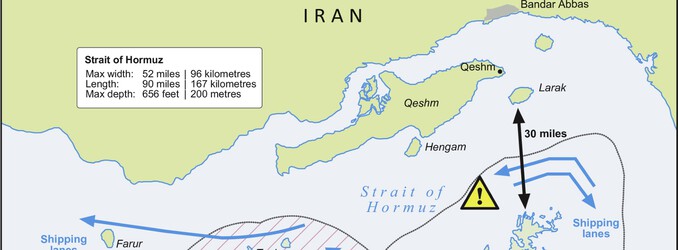

(WO) – Oil and gas executives expect disruptions in the Strait of Hormuz to persist for months and remain a recurring risk, according to the latest special questions in the Federal Reserve Bank of Dallas Energy Survey.

The first-quarter update, based on responses from 120 firms, shows most industry leaders do not expect a near-term return to normal shipping conditions. While 20% of respondents anticipate normalization by May, the largest share—39%—expects recovery to take until August, with others pointing to late 2026 or beyond.

Even after flows resume, executives see ongoing geopolitical risk. Nearly half (48%) said future disruptions in the Strait are “very likely” within the next five years, with another 38% calling them “somewhat likely.”

The disruption is expected to have lasting cost impacts. Most respondents said shipping costs from the Persian Gulf will remain elevated post-conflict, with the most common estimate falling between $2 and $4 per barrel.

On the supply side, executives anticipate only modest U.S. production gains in response to the conflict. The most common outlook for 2026 is an increase of up to 250,000 bpd, with slightly stronger growth expected in 2027.

Despite near-term disruptions, most respondents believe Gulf production losses will eventually be restored, with roughly two-thirds expecting at least 90% of shut-in volumes to return to market.

Workforce expectations remain stable. A majority of firms expect employment to hold steady through 2026, though oilfield services companies are more likely to anticipate modest hiring increases.

The survey highlights an industry outlook shaped by prolonged geopolitical uncertainty, higher operating costs and cautious production growth.

Map source: Global Energy Infrastructure.