Akzo Nobel India Ltd, popular for its Dulux paint brand, is set to become an Indian company as JSW Paints has announced the acquisition of 74.76% stake from its Dutch owner. This transaction changes the pecking order of the Indian paints industry. JSW Paints becomes the fourth largest player in terms of revenue after Asian Paints Ltd, Berger Paints India Ltd and Kansai Nerolac Paints Ltd in that order.

So, what are the implications of the deal from the perspective of non-promoter—public—shareholders of Akzo Nobel India?

JSW Paints has announced an open offer for the remaining 25.24% stake held by public shareholders at ₹3,417.77 per share. Trailing this price, Akzo’s shares closed 7% higher on Friday to ₹3,419. Now, even if a small portion of the open offer is subscribed, JSW Paints will end up having more than 75% stake as it will already be at 74.76% after the deal.

The Securities and Exchange Board of India (Sebi) mandates that promoters of listed companies cannot hold more than 75% of the shareholding in a listed entity to ensure sufficient market liquidity. If the promoter holding crosses the stipulated limit owing to a buyback, an open offer or a merger, then promoters must reduce their shareholding to 75% or below within a timeframe allowed by Sebi. So, JSW Paints will have to think of an alternative to reduce its stake.

JSW group already has JSW Steel, JSW Energy and JSW Infrastructure as three listed companies (JSW Holdings is also listed, but it has no material business), with JSW Cement’s public issue likely in the near future as it has been approved by Sebi. So, it would ideally want to list JSW Paints as well.

There’s a risk of a reverse merger for Akzo Nobel India’s shareholders on unfavourable terms. In a reverse merger, an acquiring company merges with the acquired company. This means JSW Paints might be reverse-merged with Akzo Nobel India. The possibility of an adverse merger ratio for the public shareholders of Akzo Nobel India cannot be ruled out even if independent valuers are appointed.

There are precedents available when dominant shareholders got a favourable merger ratio despite having inferior fundamentals. Cairn India was merged into Vedanta in 2017. Cairn India was a cash-rich and debt-free company, while Vedanta had high debt, but the merger terms were favourable to Vedanta as it was a dominant shareholder. Subsequently, the merger ratio was tweaked marginally to appease public shareholders of Cairn India after a hue and cry from them. But even then, concerns remained about the fair valuation of Cairn India.

That aside, JSW group’s aggressive management style might be beneficial for Akzo Nobel India’s shareholders. The group is known for inorganic growth through acquisitions. Hence, it won’t be surprising if they pursue more acquisitions of smaller players beyond the top five companies through an equity swap after JSW Paints gets listed. Indigo Paints, Shalimar Paints and Sirca Paints are some smaller companies that might be potential candidates. Equity-swap acquisitions help in bringing down the promoter stake to comply with the 25% public shareholding listing norms.

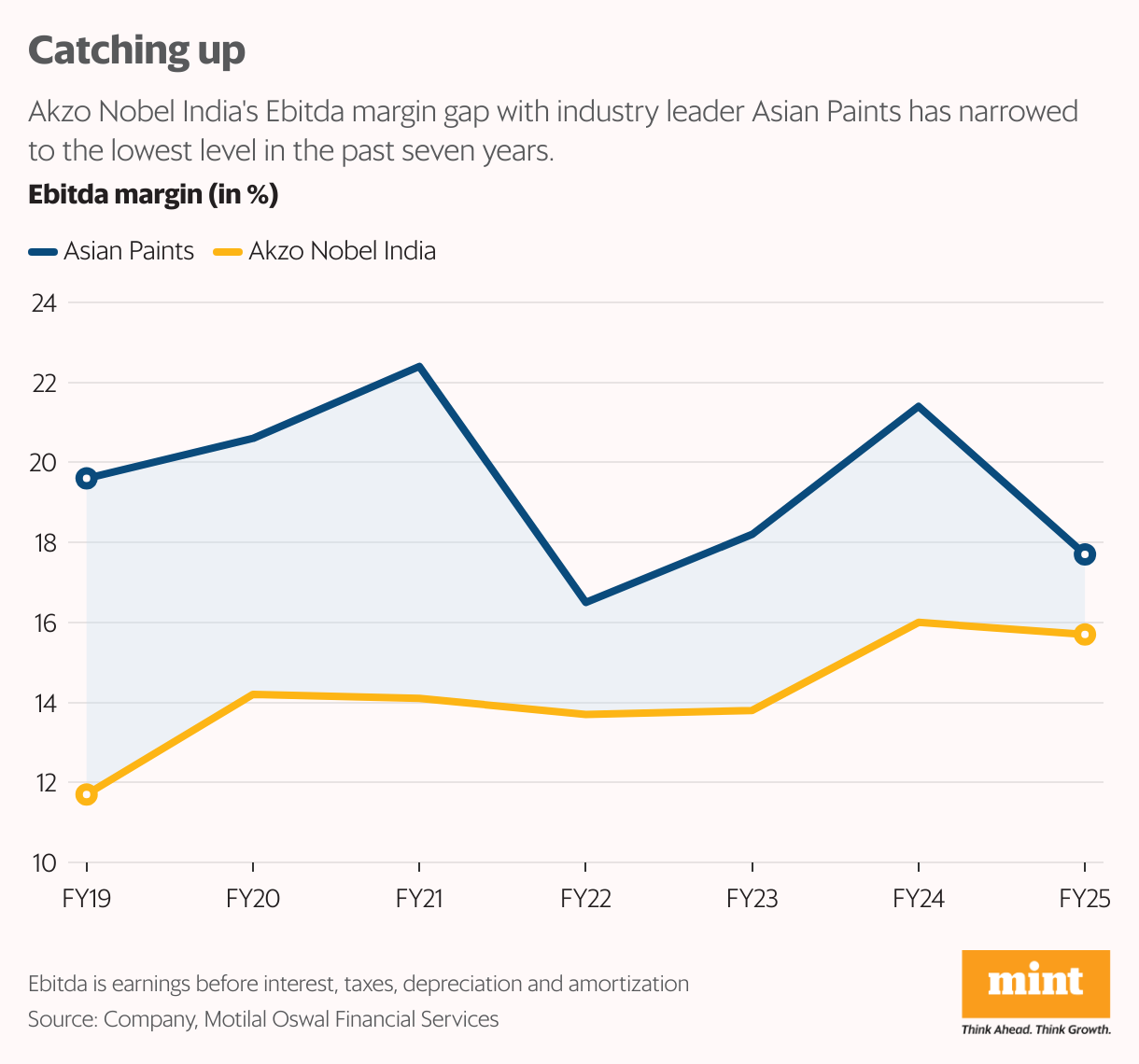

Coming to valuation, Akzo Nobel India’s public shareholders can hope for a rerating. India’s top two paint companies, Asian Paints and Berger Paints, trade at a price-to-earnings multiple of about 52-53 times, versus 36 times for Akzo Nobel India, based on Bloomberg FY26 consensus estimates. While the top two companies have a bigger presence in decorative paints, which have more brand loyalty and fetch higher margins compared to the industrial segment, the significant gap in valuation appears unwarranted.