Valued at ₹25,689 crore, this marks Torrent’s largest-ever acquisition and makes it India’s fifth-largest pharmaceutical company. Torrent is expected to gain operational control by the fourth quarter of FY26, after which synergies are likely to start taking shape.

The transaction will be executed in several phases. First, Torrent will acquire a 46.4% stake in JB Pharma for ₹11,917 crore, at ₹1,600 a share. This will trigger a mandatory open offer for up to 26% of JB Pharma’s public shareholding at a price of ₹1,639 a share.

In addition, Torrent has indicated its intent to buy up to 2.8% of the stake held by JB Pharma employees, also at the transaction price. After all this, JB Pharma will be merged into Torrent, with Torrent remaining as the surviving listed entity.

So, how will this acquisition benefit Torrent? Let’s take a closer look.

Financing the deal has a near-term cost

Torrent is expected to gain operational control of JB Chemicals by Q4FY26, and synergies will likely play out in phases.The deal is expected to be cash-accretive from the first year itself. But it is projected to be earnings accretive only from FY28, assuming 40% public ownership post-open offer.

If the open offer triggers a higher stake, earnings-per share accretion could be delayed to FY29. That said, Torrent will benefit from procurement efficiencies, expense rationalisation and manufacturing optimisation. It’s also expected to boost revenue from FY28 onwards as Torrent leverages JB’s sales representatives to drive growth.

However, some part of profitability can be offset by amortised cost, too. Centrum Broking estimates 75-80% of the acquisition cost will be amortised over 15 years. While this provides some tax benefit, it also reduces accounting profits in the medium term.

But the benefits could dent the balance sheet in the short term. As of FY25, Torrent’s cash balance was ₹579 crore, implying that the acquisition cost would need to be funded almost entirely by debt. JB Chemicals, on the other hand, has ₹130 crore of cash, taking the combined cash reserves to ₹709 crore.

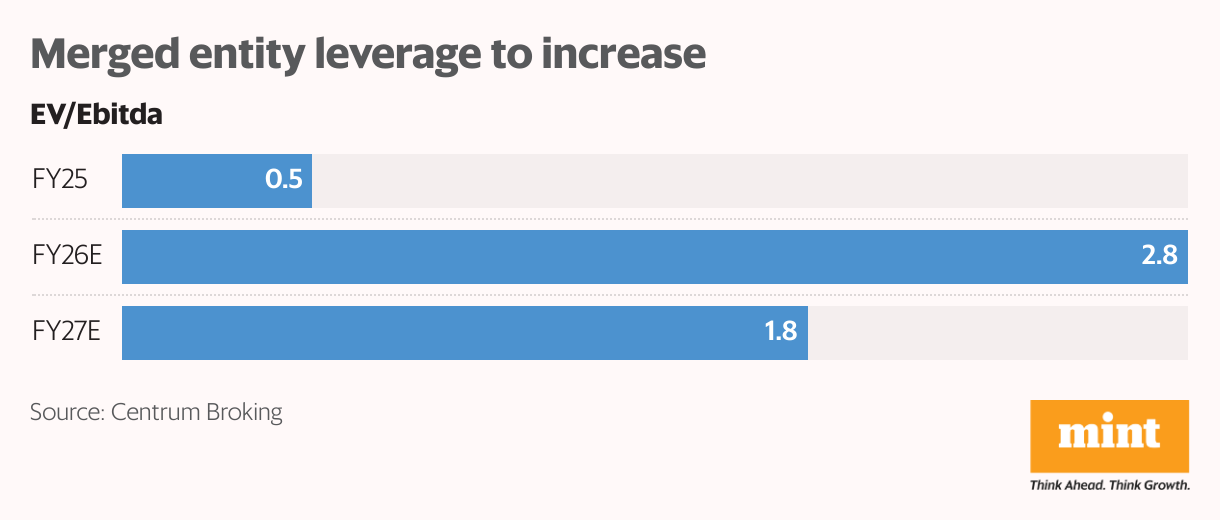

Given this limited cash buffer, Centrum estimates the net debt of the merged entity will grow from ₹2,345 crore in FY25 to ₹15,031 crore in FY26, and decline to ₹11,669 crore in the following year.

With this increase in borrowing, the net-debt-to-Ebitda will also expand from 0.5 in FY25 to 2.8 in FY26. But it will then improve to 1.8 by FY27 as cash flows improve and debt is pared down.

JB Chemicals brings growth and discipline

For Torrent, the appeal of JB Chemicals lies in its consistent performance, high-growth portfolio, and operational efficiency. JB’s revenue has nearly doubled over FY21-25, from ₹2,043 crore to ₹3,918 crore. Net profit rose 46% during the period, from ₹449 crore to ₹660 crore. The company maintained a return on capital employed (RoCE) of over 20%, signalling efficient capital deployment.

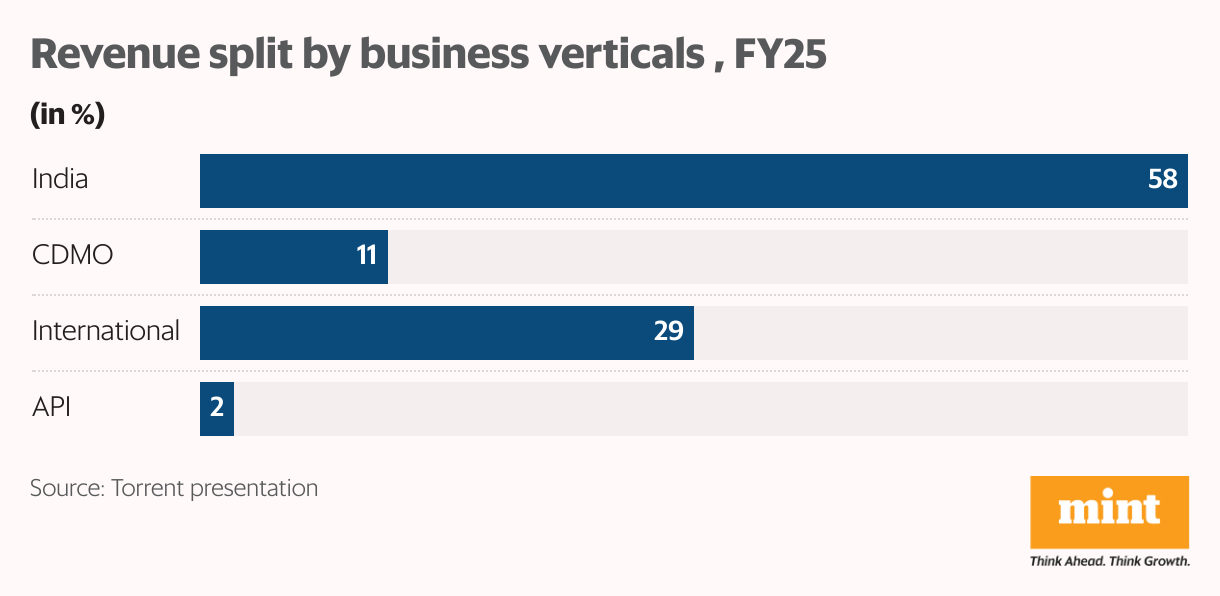

Although JB has an international presence, it remains primarily focused on the Indian market. About 58% of its revenue comes from India and the remaining 42% from exports. Within that, international formulations contribute 29%, contract development and manufacturing (CDMO) adds 11%, and APIs make up the remaining 2%. JB has carved out a niche for itself in the global lozenges-based CDMO space, serving several multinational clients.

Strong fit in therapy and brand leadership

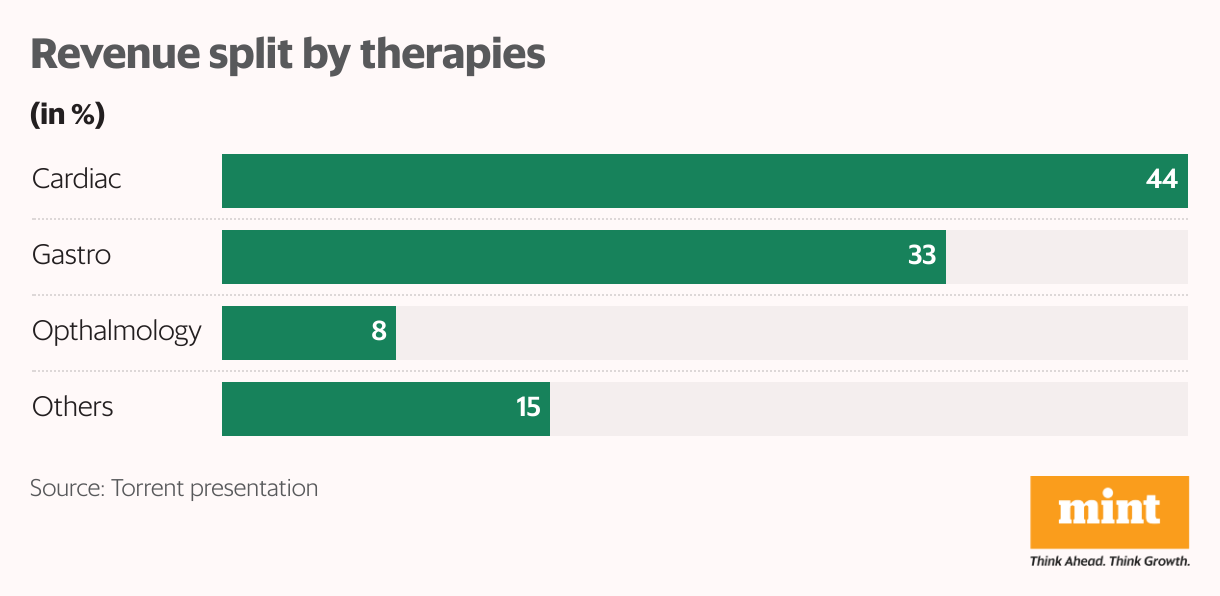

What makes JB’s business even more relevant to Torrent is the therapy mix. Its product portfolio is sharply tilted toward chronic care – cardiac and gastroenterology together contribute 77% of total revenue, while ophthalmology accounts for another 8%.

The rest spans areas such as paediatrics, IVF and nephrology. This alignment with high-growth, long-duration treatment areas gives JB a strong footing in structurally expanding segments. That strength reflects in market outperformance.

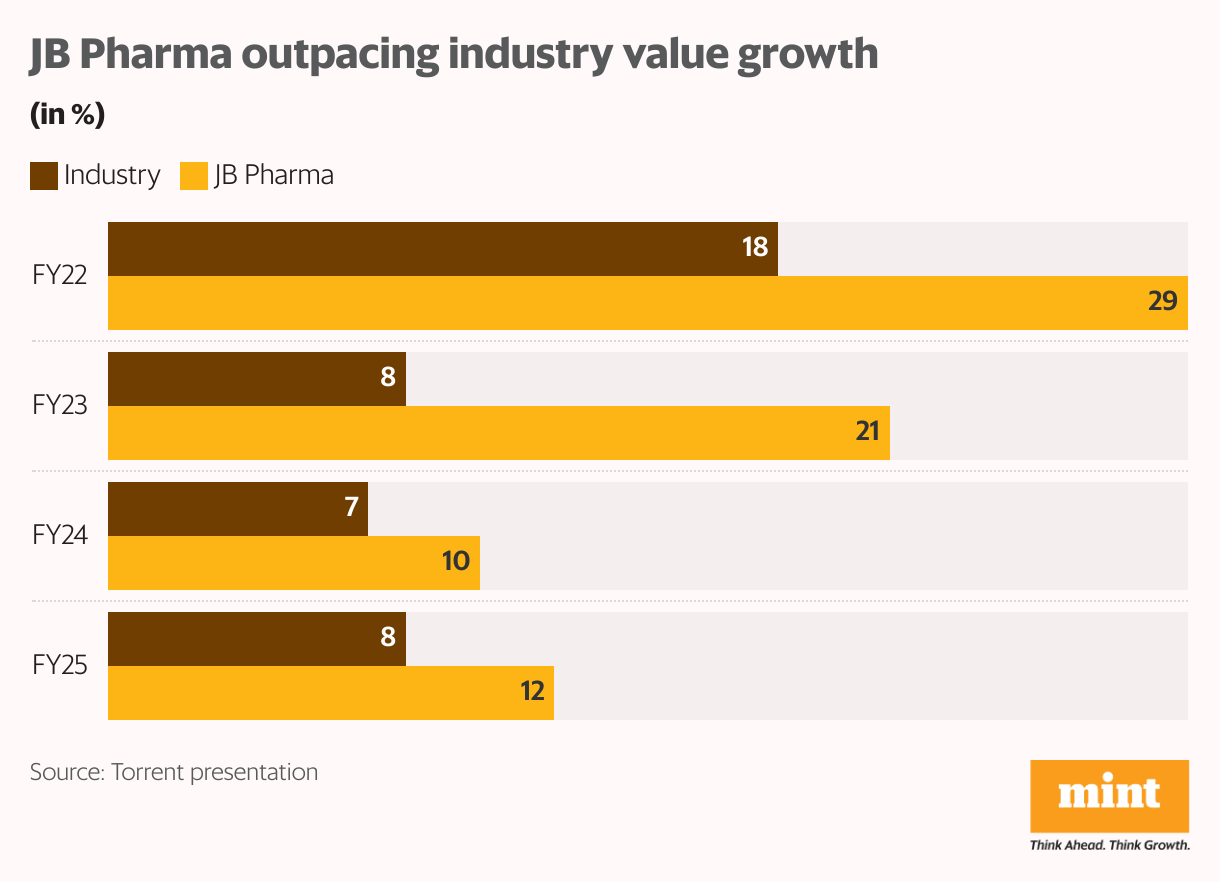

In FY25, JB’s domestic business grew by 12% in value and 4.8% in volume, outpacing industry’s growth of 8% and 1.4%, respectively. Its cardiac portfolio has expanded at a 19% compound annual growth rate (CAGR) in value terms over the past three years, almost double the industry’s 10% rate. Gastro also rose at a 12% CAGR vs industry’s 10%, and ophthalmology grew at a 10% CAGR vs the industry’s 5%.

At the brand level, JB Chemicals has built a solid franchise. Cilacar, its flagship cardiac brand, remains one of the top-selling drugs in its class. Brands such as Nicardia, Sporlac, and Metrogyl continue to hold leadership positions, reinforcing JB’s strength in high-volume, high-growth categories.

Torrent strengthens its chronic dominance

The merger will significantly reshape Torrent’s standing in the Indian pharmaceutical market. As of May 2025, JB Chemicals was ranked 22nd, while Torrent stood at seventh. After the merger, the combined entity is expected to climb to fifth in the overall rankings, with a market share of 4.8%, up from Torrent’s standalone 3.6% in Q4FY25.

Torrent is already a dominant player in chronic therapies, particularly cardiac, gastro, and paediatric. JB Chemicals complements this profile well, with overlapping strengths.

In addition, Kotak Institutional Equities estimates that about 36% of JB’s domestic sales come from molecules where Torrent already has a presence, albeit at a smaller scale. Sales from these overlaps are currently around ₹5 crore, but this will accelerate with JB’s integration.

Interestingly, the overall portfolio overlap is limited. As per IQVIA, overlapping molecules in JB’s top 55 products contribute only about 2% of combined domestic sales. This allows Torrent to enter several of JB’s strong brands and categories where its presence has been minimal. These include molecules such as cilnidipine, nifedipine, ranitidine, and metronidazole—all of which JB has scaled successfully.

Tapping new growth frontiers

Beyond the expected scale and brand synergy, the JB deal also opens up new therapeutic avenues for Torrent. The ophthalmology franchise, backed by perpetual licensing rights, offers a long runway for growth. It also provides Torrent a foothold in IVF and nephrology—segments where JB has early traction, but Torrent doesn’t.

The CDMO vertical is another significant strategic lever. JB’s strength in lozenges manufacturing adds depth to Torrent’s existing capabilities. Torrent plans to retain JB’s cost-plus model and continue investing in the platform. This vertical has a strong overseas client base, which could enhance Torrent’s export competitiveness over time.

Internationally, the combination improves reach with minimal overlap. Torrent already has a front-end in the US and Brazil. JB adds exposure to South Africa, Russia, and select emerging markets, creating a more geographically diversified revenue base.

Centrum Broking sees this broader footprint as a long-term positive, especially given the low integration risk on the product side.

What’s next?

Torrent has a proven track record of integrating acquisitions, as seen with Elder Pharma and Curatio. The JB Chemical deal takes that strategy a step further, helps deepen its presence in fast-growing chronic therapy, and opens up new therapeutic and international markets.

While the near-term increase in leverage and integration complexity warrant attention, Torrent’s past execution offers comfort. For investors, the acquisition aligns well with the company’s ambitions, even if the full benefits may take time to show up in the numbers. Torrent share price shot up 4% on 30 June, reflecting the market’s optimism.

For more such analysis, read Profit Pulse.

Madhvendra has over seven years of experience in equity markets and has cleared the NISM-Series-XV: Research Analyst Certification Examination. He specialises in writing detailed research articles on listed Indian companies, sectoral trends, and macroeconomic developments.

Disclosure: The writer does not hold the stocks discussed in this article.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.